Have you heard about what's happening right now in the Tri-Cities housing market? It's a very strong seller's market! Inventory is really low. There are a lot of buyers looking for homes to buy, and they're often competing against one another in bidding wars.

It begs the question: Is this a smart time to buy a home in the Tri-Cities?

Only you know the answer to that. The decision can be complicated. If your needs are changing, you might not have the option to stay where you are. You might have personal or professional things influencing your decision.

But outside of personal and professional factors, the real estate aspects of the decision provide a pretty clear answer. If you're deciding to buy now or wait until later in 2021, or even into next year, you need to ask yourself two questions:

1.) Do I think home values will be higher a year from now?

2.) Do I think mortgage rates will be higher a year from now?

From a purely financial standpoint, if the answer is "yes" to either question, you should strongly consider buying now. If the answer to both questions is "yes," you should definitely buy now.

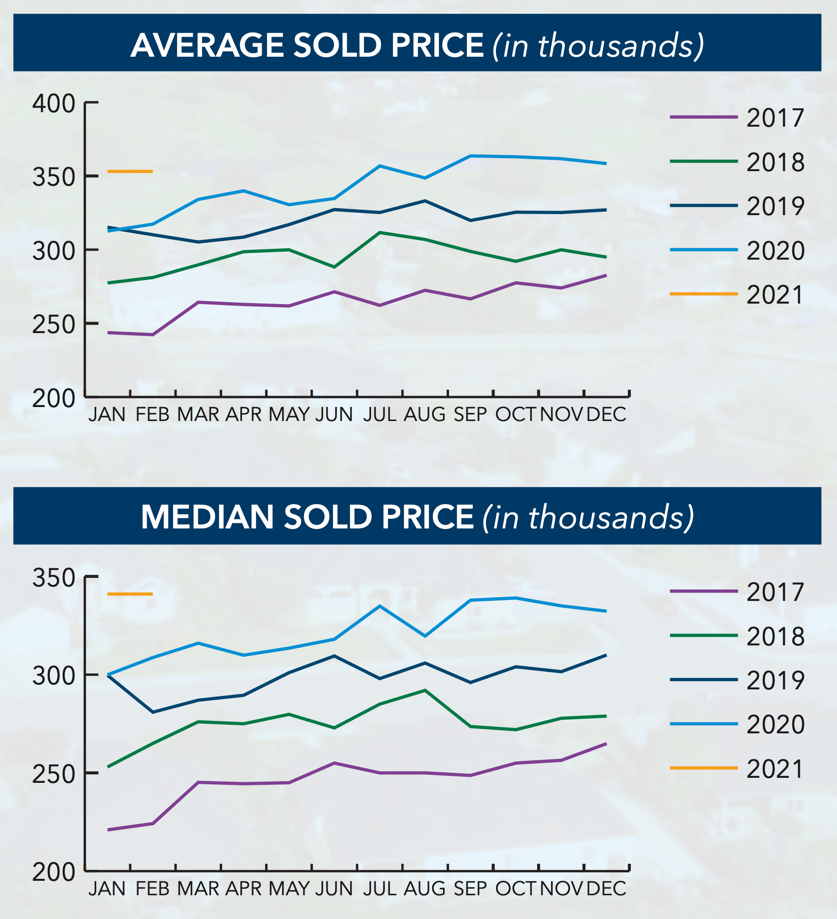

Obviously, I can't guarantee what home prices or mortgage rates will be six or 12 months from now. But take a look at these charts from the Tri-City Association of Realtors showing average and median prices since 2017:

Likewise, no one can guarantee what mortgage rates will be by the end of this year. But after reaching record lows over the past few months, rates are now rising slowly. Experts expect them to continue to rise throughout 2021.

So what does this mean to you?

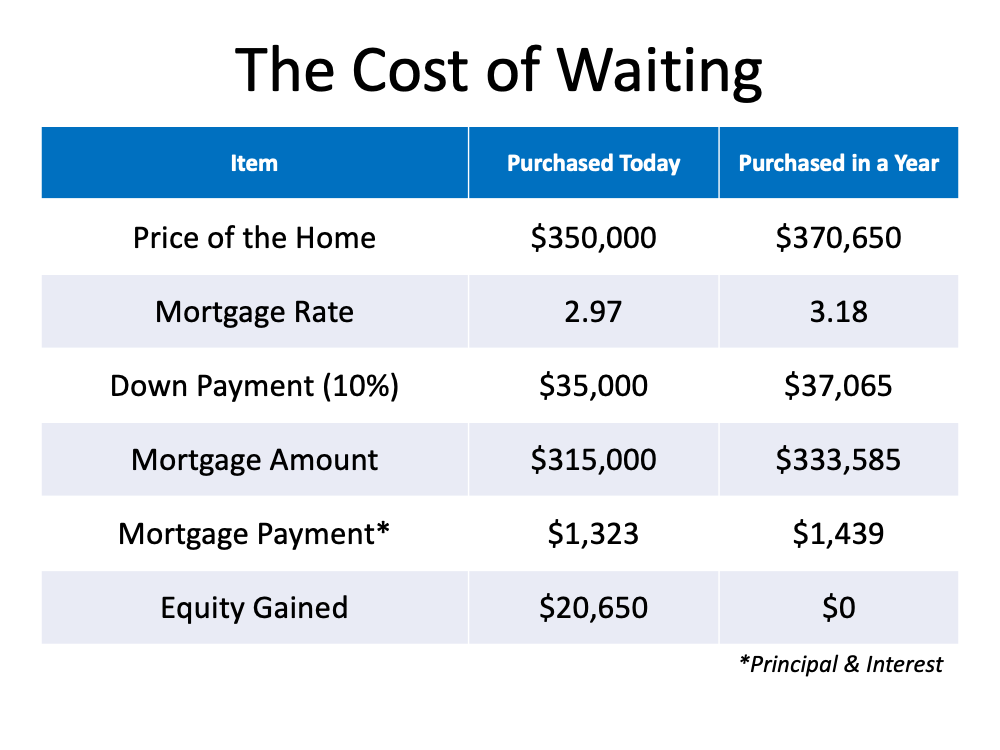

Let’s look at how waiting would impact your financial situation. Here are the assumptions made for this example:

- The experts are right - mortgage rates will be 3.18% at the end of the year

- The experts are right - home values will appreciate by 5.9%

- You want to buy a home valued at $350,000 today

- You decide on a 10% down payment

Here’s the financial impact of waiting:

- You pay an extra $20,650 for the house

- You need an additional $2,065 for a down payment

- You pay an extra $116/month in your mortgage payment ($1,392 additional per year)

- You don’t gain the $20,650 increase in wealth through equity build-up

Final Thoughts

As I said, there's a lot to consider when buying a home. Your personal and professional situation often dictates the timing of big decision like this. But, from a purely financial/real estate angle, if you find a home that meets your needs, buying now makes much more sense than buying next year.

- Cari